|

Cort's Social Studies

|

Survey Economics

|

Unit 2: Microeconomics, Consumer Demand, Supply, Market Equilibrium and Market Structure

Muslim Quarter, Xian, China

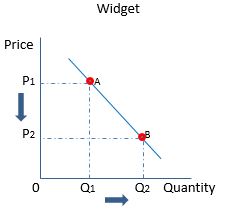

We need to distinguish between the phrases a "change in quantity demanded" and a "change in demand". Not understanding the differences leads to errors in communication and on exams. The following sections will be related to a "change in quantity demanded". Remember the term 'demand' refers to consumer buying behavior. So, a 'change in quantity demanded' refers to consumers buying more or less in response to changes in price. When we shift to a "change in demand", it will be noted.

|

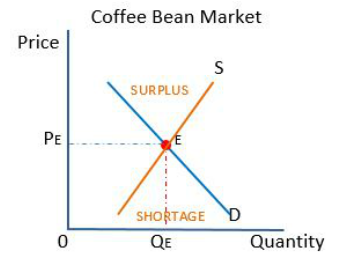

The demand curve is a graphical representation of a demand schedule showing the relationship between price and quantity demanded. (We will see demand schedules in our exercises.)

|

|

|

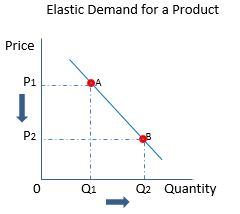

Elastic demand describes consumer behavior that clearly responds to changes in price. In the graph to the right, a decrease in price leads to a relatively large change in demand for a product. Consumer demand is clearly elastic.

|

|

|

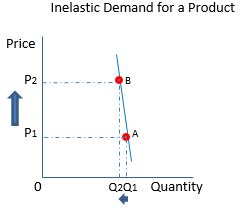

Inelastic demand describes consumer behavior that hardly responds to a change in price. In the graph to the left, a change in price leads to almost no change in buying behavior.

|

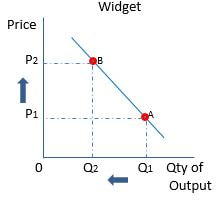

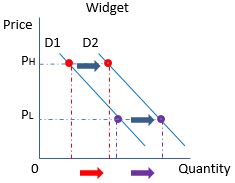

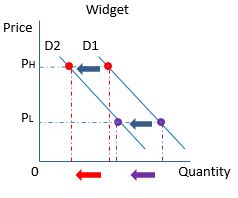

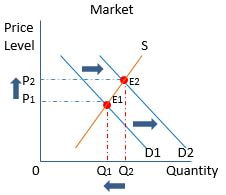

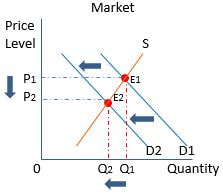

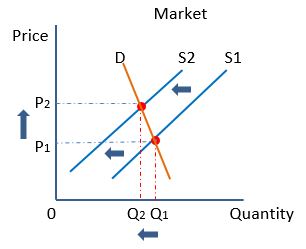

We now switch to the phrase "change in demand". Just above we identified a "change in the quantity demanded" in response to price. Remember the term 'demand' refers to consumer buying behavior. Consumer demand can change when there has been no change in price, which is referred to a 'change in demand'. The following sections refer to a change in demand for non-price reasons. Graphically this will be represented by two demand curves. One before the change and one after the change in the market.

|

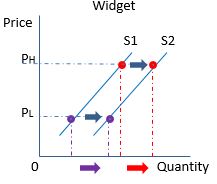

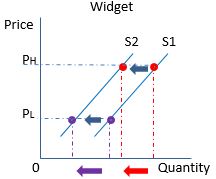

Notice in the graphs to the left, there has been no change in price for high priced (PH) or low priced (PL) widgets.

|

|

|

|

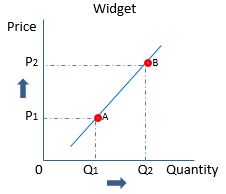

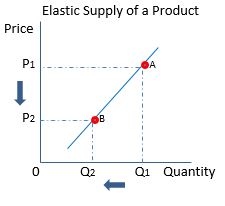

Elastic supply describes producer behavior that clearly responds to changes in price. In the graph to the right, a decrease in price leads to a relatively large change in quantity supplied of a product.

|

|

|

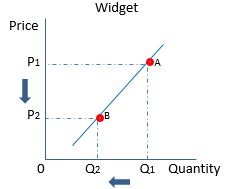

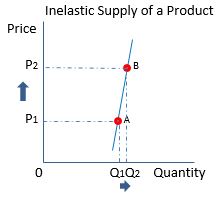

Inelastic supply describes producer behavior that hardly responds to a change in price. In the graph to the left, a change in price leads to almost no change in quantity supplied.

|

|

Notice in the graphs to the left, there has been no change in price for high priced (PH) or low priced (PL) widgets.

|

|

|

|

Regarding consumer demand, remember that there may be non-price changes in demand.

|

|

|

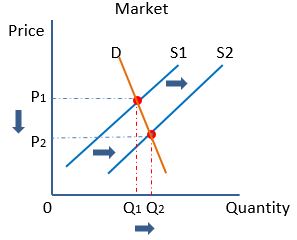

Regarding Supply, remember that there may be non-price changes in supply.

|

|

To get you to start thinking about the macroeconomic effect of market events, read the article to the left. It is an old article, but it gives an opportunity to see how one industry affects another. Now lets graph the oil and steakhouse markets.

1. Graph the Oil Market Equilibrium showing the effect of increased oil supply. 2. What will oil companies do when they see the increase in oil supply? 3. What will be the affect on oil company employees when supply increases? 4. What will happen to the demand for steak dinners at steakhouses? 5. Draw the Steakhouse Market Equilibrium showing the effect of the oil crash on demand? |

|

|

|

|

|

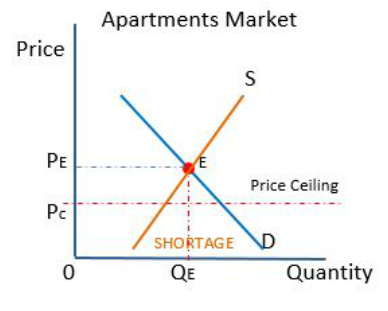

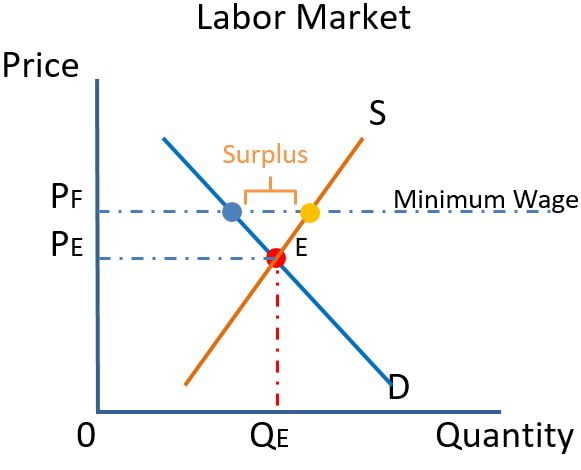

A wage is the price of labor. A minimum wage is a binding price floor on consumers of hours of labor.

|